Unsecured Business Loans: Requirements, Benefits, and Risks

Unsecured business loans can be appealing when your company needs capital but you do not want to pledge equipment, real estate, inventory, or other specific assets as collateral. For a new retailer, consultant, contractor, online store, agency, restaurant, or professional service business, that flexibility can feel like the difference between moving forward and missing an opportunity.

But “unsecured” does not mean risk-free. Many unsecured business loans still require a personal guarantee, a business lien, strong cash flow, or higher pricing to compensate the lender for taking more risk. Some fast funding options are useful in the right situation, while others can strain cash flow if the repayment schedule is too aggressive.

This guide explains what unsecured business loans are, how they work, what lenders usually require, how to compare costs, and when this type of financing may or may not be a smart choice. It is written for business owners who want plain-English guidance before signing a loan agreement.

An unsecured business loan is business financing that does not require the borrower to pledge a specific asset as collateral. Instead, the lender usually relies on the business owner’s creditworthiness, business revenue, cash flow, time in business, and sometimes a personal guarantee or general business lien.

2. What Is an Unsecured Business Loan?

An unsecured business loan is a loan or credit product made to a business without a specific collateral pledge. Unlike an equipment loan secured by a machine or a commercial mortgage secured by property, an unsecured loan is usually approved based on the overall financial strength of the business and the borrower.

Common unsecured business financing products include:

- Unsecured term loans for one-time funding needs.

- Unsecured business lines of credit for repeated access to working capital.

- Business credit cards for smaller, short-term purchases.

- Some short-term working capital loans from online lenders.

- Certain small SBA loans or SBA Express loans where collateral is not required under SBA rules for lower loan amounts.

- Invoice financing or merchant cash advances, which may not use traditional collateral but can still carry significant contractual obligations.

Reader Advice: “unsecured” usually means no specific asset is pledged upfront. It does not always mean the lender has no remedies if you default. The lender may still sue, report the default, enforce a personal guarantee, debit your business account under an ACH authorization, or rely on a general lien depending on the contract.

3. Unsecured vs. Secured Business Loans

| Feature | Unsecured Business Loan | Secured Business Loan |

|---|---|---|

| Collateral | No specific asset is pledged as collateral at approval. | A specific asset, such as equipment, inventory, receivables, cash, or real estate, secures the loan. |

| Approval focus | Credit, revenue, cash flow, business history, industry risk, and owner guarantee. | Credit and cash flow still matter, but collateral value is a major underwriting factor. |

| Typical pricing | Often higher because lender risk is higher. | Often lower when collateral is strong and liquid. |

| Funding speed | Can be faster, especially with online lenders. | May take longer due to appraisal, title work, lien filing, or collateral review. |

| Borrower risk | No pledged asset may be repossessed immediately, but personal guarantee and collections risk may remain. | Default can lead to repossession, foreclosure, liquidation, or loss of pledged assets. |

| Best for | Working capital, marketing, payroll timing gaps, inventory purchases, emergency cash flow, smaller growth projects. | Large equipment purchases, commercial real estate, vehicles, major expansion, lower-cost long-term debt. |

4. How Unsecured Business Loans Work

Unsecured business loans work like other business financing products: you apply, the lender evaluates risk, you receive funds or a credit limit, and you repay according to a contract. The difference is that the lender is not primarily relying on a pledged asset to recover money if the loan goes bad.

Most unsecured business loan decisions are based on:

- Personal and business credit history.

- Monthly or annual revenue.

- Bank account activity and average balances.

- Profitability or positive operating cash flow.

- Time in business.

- Industry risk.

- Existing debt payments.

- Tax returns, financial statements, or accounting reports.

- The intended use of funds.

- Owner experience and business stability.

Because there is no specific collateral, lenders often reduce risk in other ways. They may charge higher interest, require shorter repayment terms, ask for a personal guarantee, place a blanket UCC lien on business assets, require automatic bank withdrawals, or approve a smaller amount than the borrower requested.

5. Common Types of Unsecured Business Financing

| Type | How It Works | Best Use | Watch Out For |

|---|---|---|---|

| Unsecured term loan | You receive a lump sum and repay it over a fixed schedule. | One-time working capital, marketing, hiring, inventory, or expansion costs. | Origination fees, short terms, prepayment rules, and personal guarantees. |

| Unsecured business line of credit | You draw funds as needed up to a credit limit and pay interest on what you use. | Cash flow gaps, seasonal purchases, emergency reserves. | Draw fees, maintenance fees, variable rates, and lower limits than secured lines. |

| Business credit card | Revolving credit for purchases, subscriptions, travel, and small expenses. | Small purchases and short-term float when paid off quickly. | High APRs if balances revolve and possible personal credit impact. |

| Short-term working capital loan | Fast funding repaid over weeks or months, often with frequent payments. | Urgent needs with clear payback source. | High effective APR and cash-flow pressure. |

| Invoice financing | Advance based on unpaid B2B invoices rather than hard collateral. | Businesses waiting on customer payments. | Fees, customer payment risk, and contract complexity. |

| Merchant cash advance | Advance repaid from card sales or bank deposits, often using a factor rate. | Very limited situations where other financing is unavailable. | Can be expensive and difficult to compare with loans. Read terms carefully. |

6. Typical Requirements for Unsecured Business Loans

Requirements vary by lender and product, but most lenders look for evidence that the business can repay without relying on a pledged asset. Stronger borrowers usually receive better pricing and larger approvals.

6.1 Core Qualification Factors

- Credit profile: Many lenders review the owner’s personal credit and, if available, business credit reports.

- Revenue consistency: Lenders prefer steady deposits and predictable sales.

- Cash flow: The business should have enough money left after expenses to handle the new payment.

- Time in business: Established businesses usually qualify more easily than startups.

- Debt load: Existing loans, leases, credit cards, and cash advances reduce borrowing capacity.

- Industry and seasonality: Lenders may treat restaurants, construction, trucking, retail, and startups differently because cash flow can be volatile.

- Legal standing: The company may need to be properly registered and in good standing.

- Bank account behavior: Overdrafts, negative balances, and irregular deposits can hurt approval chances.

6.2 Documents You May Need

| Document | Why Lenders Ask for It |

|---|---|

| Business bank statements | To verify revenue, deposits, cash reserves, and overdraft patterns. |

| Tax returns | To confirm revenue, profit, and business legitimacy. |

| Profit and loss statement | To review recent sales, expenses, and net income. |

| Balance sheet | To evaluate debt, assets, equity, and liquidity. |

| Business formation documents | To confirm ownership and legal structure. |

| Government-issued ID | To verify the owner’s identity. |

| Business license or permits | To confirm the company is legally operating where required. |

| Accounts receivable aging report | Useful for invoice-based financing or B2B businesses. |

| Debt schedule | To calculate how much existing debt the business already owes. |

| Use-of-funds explanation | To understand whether the loan purpose is reasonable and likely to support repayment. |

7. Personal Guarantee vs. Collateral: A Critical Difference

A personal guarantee is a promise by the business owner to repay the debt personally if the business cannot. Many unsecured business loans require one. This means your home, savings, wages, or other personal assets may still be at risk after legal collection, even if you did not pledge a specific asset at approval.

A collateral pledge gives the lender a claim to a specific asset. A personal guarantee gives the lender a claim against you personally if the business defaults and collection is pursued. Borrowers often misunderstand this distinction.

| Term | Plain-English Meaning | Why It Matters |

|---|---|---|

| No collateral | You are not pledging a specific business or personal asset at closing. | This can reduce upfront asset risk but does not erase repayment obligations. |

| Personal guarantee | You personally promise to repay if the business does not. | Your personal finances may be exposed after default. |

| Blanket UCC lien | The lender may file a general claim against business assets. | This can affect future borrowing and asset sales. |

| ACH authorization | The lender can debit payments from your business bank account. | Daily or weekly debits can create cash-flow strain. |

| Confession of judgment | A legal document that may limit your ability to contest collection in some contexts. | Treat as a serious red flag and get legal advice before signing. |

8. Why Unsecured Business Loans Matter

Access to capital can determine whether a business can buy inventory, accept a large order, cover payroll during a temporary cash gap, replace lost revenue, or invest in growth. Unsecured financing matters because many small businesses do not own enough collateral to qualify for traditional secured loans.

At the same time, unsecured financing can be more expensive and easier to misuse. The loan may solve an immediate cash problem but create a larger repayment problem if the business lacks a clear payoff plan. The best unsecured business loan is not simply the fastest offer. It is the loan that matches the business’s cash flow, repayment ability, and purpose.

9. Benefits of Unsecured Business Loans

| Benefit | How It Helps | Best-Fit Scenario |

|---|---|---|

| No specific collateral pledge | You may not need to risk a particular asset such as equipment or property upfront. | Service businesses, online businesses, or startups with few hard assets. |

| Faster application process | Less collateral review can shorten approval and funding time. | Time-sensitive inventory, payroll, or project opportunities. |

| Flexible use of funds | Funds can often be used for many working capital needs. | Marketing, hiring, supplies, software, repairs, or cash flow gaps. |

| Can build business credit | On-time payments may help establish a stronger borrowing profile if the lender reports. | Owners planning to qualify for larger, lower-cost financing later. |

| Useful for short-term needs | A line of credit or short-term loan can bridge timing gaps. | Seasonal businesses and invoice delays. |

10. Risks and Drawbacks of Unsecured Business Loans

- Higher cost: Lenders may charge higher rates and fees because they have less collateral protection.

- Personal guarantee risk: The owner may remain personally liable even when the loan is marketed as unsecured.

- Short repayment terms: Some products require daily or weekly payments, which can pressure cash flow.

- Smaller loan amounts: Without collateral, approvals may be lower than the amount requested.

- Refinancing trap: Repeatedly borrowing to pay older debt can create a debt cycle.

- Contract complexity: Factor rates, fees, renewal fees, draw fees, and prepayment rules can make offers hard to compare.

- Bank account disruption: Automatic withdrawals can trigger overdrafts if sales drop.

- Future borrowing limitations: UCC filings or existing debt can make other lenders hesitate.

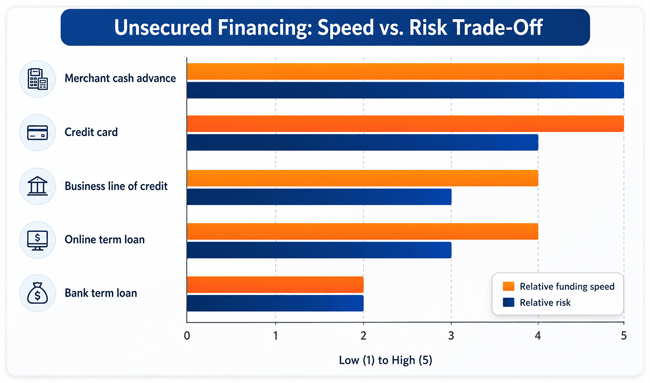

Chart: Unsecured financing often trades speed for cost and risk. This is a relative illustration, not a universal ranking.

11. Costs and Fees to Compare Before You Apply

Do not compare unsecured business loans by payment amount alone. A lower weekly payment over a longer period can still cost more than a higher payment over a shorter period. Ask each lender for the total repayment amount and, whenever possible, the annual percentage rate or estimated APR.

| Cost Item | What It Means | What to Ask |

|---|---|---|

| Interest rate or APR | The financing cost expressed as a rate. APR is usually the better comparison tool when available. | What is the APR, not just the simple rate? |

| Origination fee | A fee charged to make the loan, often deducted from proceeds or added to the balance. | Will I receive the full approved amount? |

| Draw fee | A fee charged each time you use a line of credit. | Is there a fee for every draw? |

| Maintenance fee | A monthly or annual fee for keeping a line open. | Do I pay this even if I do not draw funds? |

| Prepayment penalty | A fee or lost discount if you repay early. | Can I save interest by paying early? |

| Factor rate | A multiplier used by some advances instead of an interest rate. | What is the total dollar cost and estimated APR? |

| Late fee or returned payment fee | Fees if your payment fails or arrives late. | How much is the fee and when is it charged? |

11.1 Simple Cost Example

Suppose a business borrows $30,000 and must repay $36,000 over 12 months. The obvious cost is $6,000, but that does not automatically mean the APR is 20%. Because the balance declines over time, the effective annual cost can be higher than a simple fee divided by the original loan amount. That is why comparing total repayment, payment frequency, fees, and APR matters.

12. Step-by-Step Process to Get an Unsecured Business Loan

- Define the purpose of the loan. Write down exactly how the funds will be used and how the use will help revenue, stability, or efficiency.

- Estimate the affordable payment. Review monthly cash flow and decide what payment your business can handle during a weak month, not just an average month.

- Check personal and business credit. Correct errors, pay down revolving balances where possible, and avoid unnecessary new credit applications.

- Gather documents. Prepare bank statements, tax returns, financial statements, ownership records, and a debt schedule.

- Compare at least three offers. Include banks, credit unions, online lenders, and lines of credit where appropriate.

- Request total cost details. Ask for APR, total repayment, all fees, payment frequency, term length, personal guarantee requirements, and lien terms.

- Read the contract slowly. Look for automatic withdrawals, default triggers, prepayment rules, renewal language, and collection remedies.

- Use funds for the planned purpose. Avoid using loan proceeds to cover ongoing losses unless you also have a turnaround plan.

- Track repayment impact. Monitor cash flow weekly after funding and adjust spending before payments become stressful.

13. Real-World Examples

13.1 Example 1: Seasonal retail inventory

A boutique needs $20,000 to buy holiday inventory before sales arrive. A revolving unsecured business line of credit may fit better than a term loan because the owner can draw only what is needed and repay after the season. The key risk is overbuying inventory and carrying debt into the slow season.

13.2 Example 2: Contractor waiting on invoices

A contractor has completed work but will not be paid for 45 days. An unsecured working capital loan may cover payroll, but invoice financing may better match the repayment source if the invoices are strong. The owner should compare fees and confirm what happens if the customer pays late.

13.3 Example 3: Restaurant with unstable sales

A restaurant receives a fast offer with daily withdrawals. The funding solves an immediate supplier bill, but daily payments could drain the account during slow weeks. A smaller line of credit, vendor payment plan, or expense reduction may be safer than a high-cost advance.

13.4 Example 4: Professional services firm expanding marketing

A consulting firm with stable revenue wants to spend $15,000 on a marketing campaign. If the campaign has a realistic payback timeline, an unsecured term loan with fixed monthly payments can be reasonable. The owner should avoid borrowing based only on optimistic revenue projections.

14. When an Unsecured Business Loan May Be a Good Idea

- You have a clear, specific use for the money.

- The loan supports revenue, protects operations, or bridges a temporary cash gap.

- Your business can afford the payment even if sales drop.

- You understand the total cost and repayment schedule.

- You are not using new debt mainly to delay an unavoidable cash-flow problem.

- The contract does not include terms you do not understand or cannot accept.

15. When to Avoid or Pause Before Borrowing

- You cannot explain how the loan will be repaid.

- The payment would require perfect sales every week.

- You are already using one loan to pay another.

- The lender will not clearly disclose total repayment and fees.

- The contract includes aggressive collection terms you do not understand.

- You feel pressured to sign immediately.

- Your business is losing money and has no plan to become profitable.

16. Unsecured Business Loan Alternatives

| Alternative | When It May Be Better | Main Trade-Off |

|---|---|---|

| Secured business loan | You have valuable collateral and want lower pricing or a larger amount. | Specific assets may be at risk. |

| SBA loan | You can wait longer and meet eligibility and documentation requirements. | More paperwork and lender review. |

| Invoice financing | You have unpaid B2B invoices from reliable customers. | Fees and customer-payment dependency. |

| Equipment financing | You are buying equipment that can secure the loan. | Funds are tied to the equipment purchase. |

| Vendor terms | You need inventory or supplies and can negotiate payment timing. | May be limited by supplier relationship. |

| Business grant | You qualify for a specific program and can wait. | Competitive and not guaranteed. |

| Owner contribution | You can safely invest more equity. | Personal funds are at risk. |

| Expense restructuring | The cash gap is caused by recurring overspending. | Requires operational discipline, not just financing. |

17. Expert Tips for Choosing the Best Unsecured Business Loan

- Match the loan term to the use of funds. Do not finance a short-lived expense over a long period unless there is a clear reason.

- Compare total repayment, not just approval amount.

- Ask whether the lender reports positive payments to business credit bureaus.

- Avoid stacking multiple short-term loans or advances.

- Keep a cash reserve equal to at least several payment cycles when possible.

- Do not sign a personal guarantee casually. Treat it as a serious financial obligation.

- Use conservative revenue projections. If the loan works only in the best-case scenario, it may be too risky.

- Ask a CPA, attorney, or trusted financial advisor to review complex contracts, especially advances and agreements with unusual collection terms.

18. Common Mistakes to Avoid

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Assuming unsecured means no personal risk | A personal guarantee can still expose the owner. | Read guarantee and default clauses carefully. |

| Comparing only monthly payment | Fees, term length, and payment frequency change true cost. | Compare APR, total repayment, and cash-flow impact. |

| Borrowing without a use-of-funds plan | Debt may disappear into daily expenses without solving the problem. | Tie each dollar to a specific business purpose. |

| Ignoring daily or weekly withdrawals | Frequent payments can create overdrafts. | Stress-test repayment during low-sales periods. |

| Taking the first fast offer | Speed can come with high cost or harsh terms. | Compare several lenders before signing. |

| Using debt to cover chronic losses | Borrowing can delay but not fix an unprofitable model. | Repair pricing, costs, staffing, or operations first. |

| Not checking for liens or guarantees | Future financing can be harder if a lender files a UCC lien. | Ask what filings or guarantees are required. |

19. Quick Action Checklist

- Write the exact loan purpose in one sentence.

- Calculate the maximum payment your business can handle in a weak month.

- Gather the last three to six months of bank statements.

- Review personal and business credit reports where available.

- List all existing business debts and payment amounts.

- Request APR, total repayment, fees, term, payment frequency, personal guarantee language, and lien details from each lender.

- Compare at least three offers side by side.

- Read the default and collections sections of the contract.

- Do not borrow more than the business can repay from realistic cash flow.

- Set calendar reminders for payment dates and review cash flow weekly after funding.

20. Frequently Asked Questions About Unsecured Business Loans

20.1 What is an unsecured business loan?

An unsecured business loan is financing that does not require a specific asset as collateral. The lender usually relies on credit, revenue, cash flow, business history, and often a personal guarantee.

20.2 Can I get a business loan with no collateral?

Yes, some lenders offer business loans without specific collateral. However, you may still need strong revenue, acceptable credit, and a personal guarantee.

20.3 Are unsecured business loans hard to get?

They can be harder to qualify for than secured loans if your credit, revenue, or cash flow is weak. Since the lender has less collateral protection, underwriting may focus heavily on repayment ability.

20.4 Do unsecured business loans require a personal guarantee?

Many do. A personal guarantee means you may be personally responsible if the business cannot repay. Always check the contract before assuming your personal assets are protected.

20.5 What credit score is needed for an unsecured business loan?

There is no single universal score requirement. Banks usually prefer stronger credit, while some online lenders may consider lower credit if revenue and cash flow are strong.

20.6 Can startups get unsecured business loans?

Some startups can qualify, but it is more difficult without operating history or revenue. Startup owners may rely on business credit cards, personal credit, grants, microloans, or owner equity.

20.7 How much can I borrow with an unsecured business loan?

Loan amounts depend on revenue, cash flow, credit profile, time in business, debt load, industry, and lender policy. Without collateral, approvals may be smaller than secured loan approvals.

20.8 Are unsecured business loans expensive?

They can be more expensive than secured loans because the lender takes more risk. Costs vary widely, so compare APR, total repayment, fees, term length, and payment frequency.

20.9 Is a business line of credit unsecured?

Some business lines of credit are unsecured, while others are secured by receivables, inventory, cash, or other assets. Read the agreement to confirm whether collateral or a UCC lien is required.

20.10 What happens if I default on an unsecured business loan?

The lender may charge fees, report the default, accelerate the balance, debit authorized accounts, enforce a personal guarantee, sue, or use collection remedies allowed by the contract and law.

20.11 Is an unsecured business loan better than a credit card?

It depends on the amount, purpose, cost, and repayment timeline. A loan may be better for larger planned expenses, while a card may work for small purchases paid off quickly.

20.12 Can unsecured business loans build business credit?

They may help if the lender reports payment history to business credit bureaus and you pay on time. Ask the lender whether it reports before you apply.

20.13 What is the safest unsecured financing option?

The safest option is usually the lowest-cost product with payments your business can afford from realistic cash flow. For many businesses, that may be a bank line of credit, credit union loan, or transparent online loan rather than a high-cost advance.

20.14 Should I use an unsecured loan to pay old business debt?

Be careful. Refinancing can help if it lowers cost or improves cash flow, but borrowing just to delay default can worsen the problem. Compare total cost and address the root cause of the debt.

20.15 How do I compare unsecured business loan offers?

Compare APR, total repayment, fees, payment frequency, term length, prepayment rules, personal guarantee language, lien filings, and default remedies. Do not rely on the advertised rate alone.

21. Authoritative Notes and Trust Signals

The SBA states that 7(a) loan applicants generally must be operating for profit, located in the United States, small under SBA size standards, unable to obtain desired credit on reasonable terms from non-government sources, creditworthy, and able to repay. SBA guidance for 7(a) Small loans and SBA Express loans also says collateral is not required for loans up to $50,000, with lender policies applying above that threshold in specified ways.

The CFPB’s small business lending rulemaking page explains that Section 1071 of the Dodd-Frank Act amended the Equal Credit Opportunity Act to require collection and reporting of certain small-business credit application data, with a revised final rule issued May 1, 2026 and compliance extended to January 1, 2028 for covered institutions.

The FTC has warned that small business financing can involve confusing terms, inconsistent terminology, deceptive marketing, unauthorized withdrawals, and aggressive collection practices. This is especially important when comparing fast online financing, brokered products, and merchant cash advances.

22. Conclusion: The Smart Way to Use Unsecured Business Financing

Unsecured business loans can be useful when your business needs capital and does not have, or does not want to pledge, specific collateral. They can fund working capital, inventory, marketing, payroll timing gaps, short-term opportunities, and emergency needs. Their main advantage is flexibility; their main danger is assuming “unsecured” means “safe.”

Before applying, focus on repayment ability, total cost, contract terms, and realistic cash flow. Avoid borrowing because approval is easy or fast. Borrow because the money has a clear business purpose, the repayment schedule fits your numbers, and the benefit outweighs the cost.

The best next step is simple: compare offers carefully, read every guarantee and lien clause, and choose financing that strengthens your business instead of putting pressure on it.

22.1 Sources Consulted

- U.S. Small Business Administration, 7(a) loans: https://www.sba.gov/funding-programs/loans/7a-loans

- U.S. Small Business Administration, Types of 7(a) loans: https://www.sba.gov/partners/lenders/7a-loan-program/types-7a-loans

- Consumer Financial Protection Bureau, Small business lending rulemaking: https://www.consumerfinance.gov/1071-rule/

- Federal Trade Commission, Small business financing staff perspective: https://www.ftc.gov/business-guidance/blog/2020/02/small-business-financing-staff-perspective-outlines-issues

- Federal Trade Commission, Protecting small businesses seeking financing: https://www.ftc.gov/business-guidance/blog/2020/08/protecting-small-businesses-seeking-financing-during-pandemic

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.